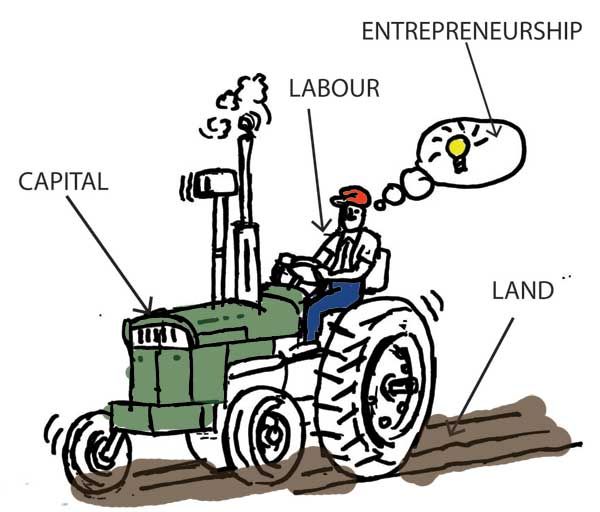

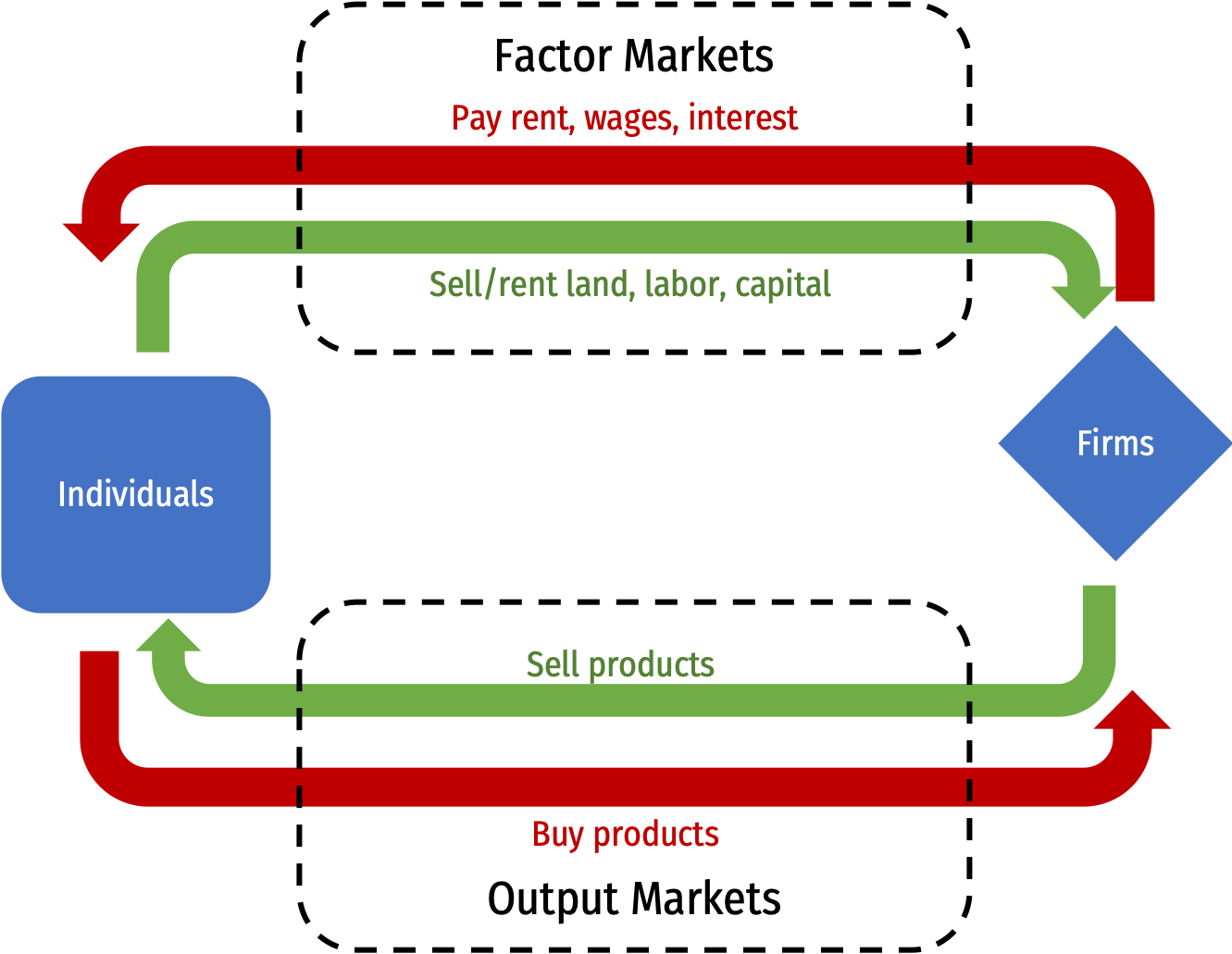

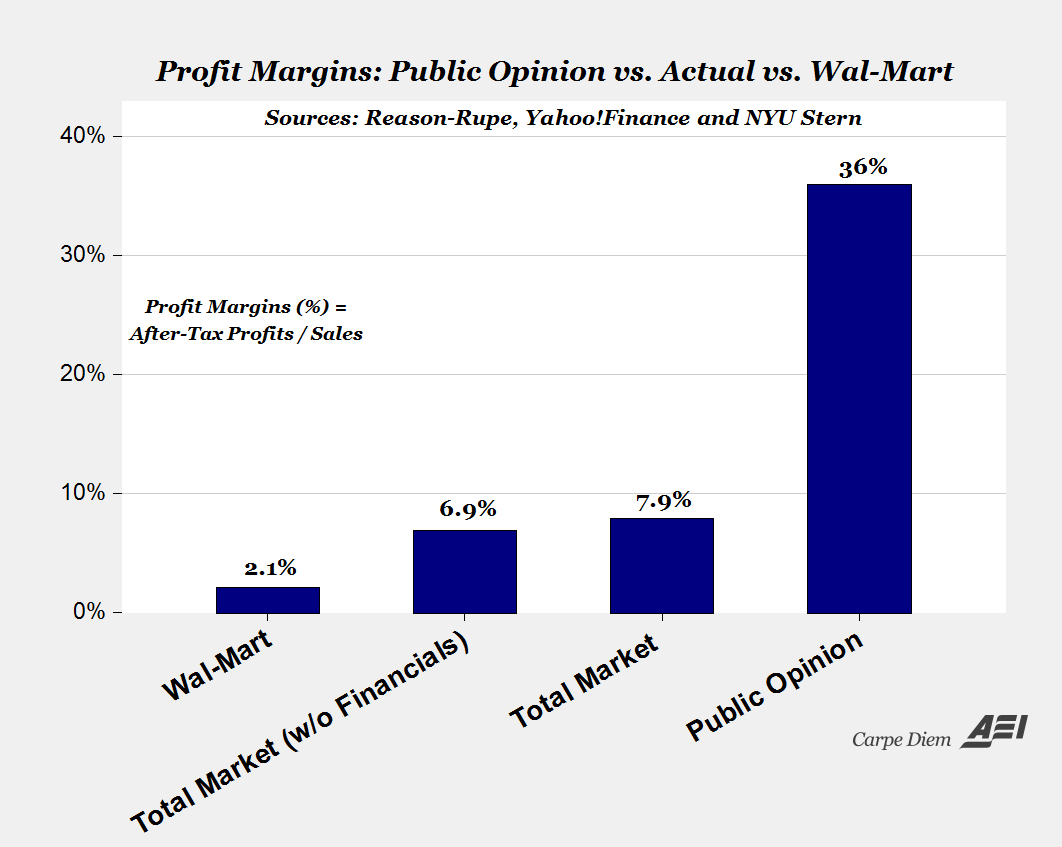

class: title-slide # 1.2 — Technology and Cost ## ECON 326 • Industrial Organization • Spring 2023 ### Ryan Safner<br> Associate Professor of Economics <br> <a href="mailto:safner@hood.edu"><i class="fa fa-paper-plane fa-fw"></i>safner@hood.edu</a> <br> <a href="https://github.com/ryansafner/ioS23"><i class="fa fa-github fa-fw"></i>ryansafner/ioS23</a><br> <a href="https://ioS23.classes.ryansafner.com"> <i class="fa fa-globe fa-fw"></i>ioS23.classes.ryansafner.com</a><br> --- class: inverse # Outline ### [Short Run Production Concepts](#27) ### [Costs in the Short Run](#37) ### [Costs in the Long Run](#65) ### [Revenues](#75) --- # This Black Box We Call "Firms" .pull-left[ - .hi[Firm] is a mere .hi-purple[production process]: - a bundle of technology, physical assets, and individuals - Synonymous with .hi[production function] - Fully replicable - We'll explore (and explode) this much later ] .pull-right[ .center[  ] ] --- # What Do Firms Do? I .pull-left[ - We'll assume “the firm” is the agent to model: - So what do firms do? - How would we set up an optimization model: 1. **Choose:** .hi-blue[ < some alternative >] 2. **In order to maximize:** .hi-green[< some objective >] 3. **Subject to:** .hi-red[< some constraints >] ] .pull-right[ .center[  ] ] --- # What Do Firms Do? II .pull-left[ .smaller[ - Firms convert some goods to other goods: ] ] .pull-right[ .center[  ] ] --- # What Do Firms Do? II .pull-left[ .smaller[ - Firms convert some goods to other goods: - **Inputs**: `\(x_1, x_2, \cdots, x_n\)` - <span class="green">**Examples**: worker efforts, warehouse space, electricity, loans, oil, cardboard, fertilizer, computers, software programs, etc<span> ] ] .pull-right[ .center[  ] ] --- # What Do Firms Do? II .pull-left[ .smaller[ - Firms convert some goods to other goods: - **Inputs**: `\(x_1, x_2, \cdots, x_n\)` - <span class="green">**Examples**: worker efforts, warehouse space, electricity, loans, oil, cardboard, fertilizer, computers, software programs, etc<span> - **Output**: `\(q\)` - <span class="green">**Examples**: gas, cars, legal services, mobile apps, vegetables, consulting advice, financial reports, etc<span> ] ] .pull-right[ .center[  ] ] --- # What Do Firms Do? III .pull-left[ - .hi[Technology] or a .hi[production function]: rate at which firm can convert specified **inputs** `\((x_1, x_2, \cdots, x_n)\)` into **output** `\((q)\)` `$$q=f(x_1, x_2, \cdots, x_n)$$` ] .pull-right[ .center[  ] ] --- # Production Function as Recipe .pull-left[ .center[The production function  ] ] .pull-right[ .center[The production algorithm  ] ] --- # Factors of Production I `$$q=A \,f(t,l,k)$$` .pull-left[ .smaller[ - Economists typically classify inputs, called the .hi[“factors of production” (FOP)]: <table> <thead> <tr> <th style="text-align:left;"> Factor </th> <th style="text-align:left;"> Owned By </th> <th style="text-align:left;"> Earns </th> </tr> </thead> <tbody> <tr> <td style="text-align:left;"> Land (t) </td> <td style="text-align:left;"> Landowners </td> <td style="text-align:left;"> Rent </td> </tr> <tr> <td style="text-align:left;"> Labor (l) </td> <td style="text-align:left;"> Laborers </td> <td style="text-align:left;"> Wages </td> </tr> <tr> <td style="text-align:left;"> Capital (k) </td> <td style="text-align:left;"> Capitalists </td> <td style="text-align:left;"> Interest </td> </tr> </tbody> </table> ] .smallest[ - `\(A\)`: .b["total factor productivity"] (ideas/knowledge/institutions) ] ] .pull-right[ .center[  ] ] --- # Factors of Production II `$$q=f(l,k)$$` .pull-left[ - We will assume just two inputs: labor `\(l\)` and capital `\(k\)` <table> <thead> <tr> <th style="text-align:left;"> Factor </th> <th style="text-align:left;"> Owned By </th> <th style="text-align:left;"> Earns </th> </tr> </thead> <tbody> <tr> <td style="text-align:left;"> Labor (l) </td> <td style="text-align:left;"> Laborers </td> <td style="text-align:left;"> Wages </td> </tr> <tr> <td style="text-align:left;"> Capital (k) </td> <td style="text-align:left;"> Capitalists </td> <td style="text-align:left;"> Interest </td> </tr> </tbody> </table> ] .pull-right[ .center[  ] ] --- # What Does a Firm Maximize? .pull-left[ - We assume firms .hi-purple[maximize profit `\\((\pi)\\)`] - Not true for all firms - <span class="green">**Examples**: non-profits, charities, civic associations, government agencies, criminal organizations, etc</span> - Even profit-seeking firms may also want to maximize *additional* things - <span class="green">**Examples**: goodwill, sustainability, social responsibility, etc </span> ] .pull-right[ .center[  ] ] --- # Profits Have a Bad Rap These Days .center[  ] --- # What is Profit? .pull-left[ - In economics, .hi-purple[profit] is simply **benefits minus (opportunity) costs** ] .pull-right[ .center[  ] ] --- # What is Profit? .pull-left[ - In economics, .hi-purple[profit] is simply **benefits minus (opportunity) costs** - Suppose firm sells **output** `\(q\)` at price `\(p\)` ] .pull-right[ .center[  ] ] --- # What is Profit? .pull-left[ - In economics, .hi-purple[profit] is simply **benefits minus (opportunity) costs** - Suppose firm sells **output** `\(q\)` at price `\(p\)` - It can buy each **input** `\(x_i\)` at an associated price `\(p_i\)`, i.e. - labor `\(l\)` at wage rate `\(w\)` - capital `\(k\)` at rental rate `\(r\)` ] .pull-right[ .center[  ] ] --- # What is Profit? .pull-left[ - In economics, .hi-purple[profit] is simply **benefits minus (opportunity) costs** - Suppose firm sells **output** `\(q\)` at price `\(p\)` - It can buy each **input** `\(x_i\)` at an associated price `\(p_i\)`, i.e. - labor `\(l\)` at wage rate `\(w\)` - capital `\(k\)` at rental rate `\(r\)` - The profit of selling `\(q\)` units and using inputs `\(l,k\)` is: ] .pull-right[ .center[  ] ] --- # Who Gets the Profits? I .pull-left[ `$$\pi=\underbrace{pq}_{revenues}-\underbrace{(wl+rk)}_{costs}$$` ] .pull-right[ .center[  ] ] --- # Reminder from Macroeconomics: “The Circular Flow” .center[  ] --- # Who Gets the Profits? I .pull-left[ `$$\pi=\underbrace{pq}_{revenues}-\underbrace{(wl+rk)}_{costs}$$` - .hi-purple[The firm's costs are all of the factor-owner's incomes!] - Landowners, laborers, creditors are all paid rent, wages, and interest, respectively ] .pull-right[ .center[  ] ] --- # Who Gets the Profits? I .pull-left[ `$$\pi=\underbrace{pq}_{revenues}-\underbrace{(wl+rk)}_{costs}$$` - Profits are the .hi-purple[residual value] leftover after paying all factors - Profits are income for the .hi[residual claimant(s)] of the production process (i.e. **owner(s)** of a firm): - Entrepreneurs - Shareholders ] .pull-right[ .center[  ] ] --- # Who Gets the Profits? II .pull-left[ `$$\pi=\underbrace{pq}_{revenues}-\underbrace{(wl+rk)}_{costs}$$` - Residual claimants have incentives to maximize firm's profits, as this *maximizes their own income* - Entrepreneurs and shareholders are the only participants in production that are *not* guaranteed an income! - Starting and owning a firm is inherently **risky**! ] .pull-right[ .center[  ] ] --- # People Overestimate Profits .center[  ] .source[Source: [American Enterprise Institute](https://www.aei.org/carpe-diem/the-public-thinks-the-average-company-makes-a-36-profit-margin-which-is-about-5x-too-high-part-ii/)] --- # Profits and Entrepreneurship: A Preview .pull-left[ - In markets, production must face the .hi[profit test]: - <span class="hi-purple">Is consumer's willingness to pay `\(>\)` opportunity cost of inputs?</span> - Profits are an indication that **value is being created for society** - Losses are an indication that **value is being destroyed for society** - Survival in markets *requires* firms continually create value & earn profits ] .pull-right[ .center[  ] ] --- # The Firm's Optimization Problem I .pull-left[ - So what do firms do? 1. **Choose:** .hi-blue[ < some alternative >] 2. **In order to maximize:** .hi-green[< profits >] 3. **Subject to:** .hi-red[< technology >] - We've so far assumed they maximize profits and they are limited by their technology ] .pull-right[ .center[  ] ] --- # The Firm's Optimization Problem II .pull-left[ - What do firms **choose**? (Not an easy answer) - Prices? - Depends on the market the firm is operating in! - Study of <span class="hi">industrial organization</span> - Essential question: .hi-turquoise[how competitive is a market?] This will influence what firms (can) do ] .pull-right[ .center[  ] ] --- class: inverse, center, middle # Short-Run Production Concepts --- # Marginal Products .pull-left[ - The .hi[marginal product] of an input is the *additional* output produced by *one more unit* of that input (*holding all other inputs constant*) - Like marginal utility - Similar to marginal utilities, I will give you the marginal product equations ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-3-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Marginal Product of Labor .pull-left[ - .hi[Marginal product of labor `\\((MP_l)\\)`]: additional output produced by adding one more unit of labor (holding `\(k\)` constant) `$$MP_l = \frac{\Delta q}{\Delta l}$$` - `\(MP_l\)` is slope of `\(TP\)` at each value of `\(l\)`! - Note: via calculus: `\(\frac{\partial q}{\partial l}\)` ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-4-1.png" width="504" style="display: block; margin: auto;" /> <img src="1.2-slides_files/figure-html/unnamed-chunk-5-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Marginal Product of Capital .pull-left[ - .hi[Marginal product of capital `\\((MP_k)\\)`]: additional output produced by adding one more unit of capital (holding `\(l\)` constant) `$$MP_k = \frac{\Delta q}{\Delta k}$$` - `\(MP_k\)` is slope of `\(TP\)` at each value of `\(k\)`! - Note: via calculus: `\(\frac{\partial q}{\partial k}\)` - Note we don't consider capital in the short run! ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-6-1.png" width="504" style="display: block; margin: auto;" /> <img src="1.2-slides_files/figure-html/unnamed-chunk-7-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Diminishing Returns .pull-left[ - .hi-purple[Law of Diminishing Returns]: adding more of one factor of production **holding all others constant** will result in successively lower increases in output - In order to increase output, firm will need to increase *all* factors! ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-8-1.png" width="504" style="display: block; margin: auto;" /> <img src="1.2-slides_files/figure-html/unnamed-chunk-9-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Diminishing Returns .pull-left[ - .hi-purple[Law of Diminishing Returns]: adding more of one factor of production **holding all others constant** will result in successively lower increases in output - In order to increase output, firm will need to increase *all* factors! .center[  ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-10-1.png" width="504" style="display: block; margin: auto;" /> <img src="1.2-slides_files/figure-html/unnamed-chunk-11-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Average Product of Labor (and Capital) .pull-left[ - .hi[Average product of labor `\\((AP_l)\\)`]: total output per worker `$$AP_l = \frac{q}{l}$$` - A measure of *labor productivity* - .hi[Average product of capital `\\((AP_k)\\)`]: total output per unit of capital `$$AP_k = \frac{q}{k}$$` ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-12-1.png" width="504" style="display: block; margin: auto;" /> <img src="1.2-slides_files/figure-html/unnamed-chunk-13-1.png" width="504" style="display: block; margin: auto;" /> ] --- class: inverse, center, middle # The Firm's Problem: Long Run --- # The Long Run .pull-left[ - In the long run, *all* factors of production are .hi-purple[variable] `$$q=f(k,l)$$` - Can build more factories, open more storefronts, rent more space, invest in machines, etc. - So the firm can choose both `\(l\)` *and* `\(k\)` ] .pull-right[ .center[  ] ] --- # Production Costs are Opportunity Costs .pull-left[ - Remember, .hi[economic costs] are broader than the common conception of “cost” - .hi-purple[Accounting cost]: monetary cost - .hi[Economic cost]: value of next best alternative use of resources given up (i.e. .hi[opportunity cost]) ] .pull-right[ .center[   ] ] --- # Production Costs are Opportunity Costs .pull-left[ - This leads to the difference between: - .hi-purple[Accounting profit]: revenues minus accounting costs - .hi[Economic profit]: revenues minus accounting + .ul[opportunity] costs - A really difficult concept to think about! ] .pull-right[ .center[   ] ] --- # Production Costs are Opportunity Costs .pull-left[ - Another helpful perspective: - .hi-purple[Accounting cost]: what you **historically** paid for a resource - .hi[Economic cost]: what you can **currently** get in the market for a selling a resource (it’s value in *alternative* uses) ] .pull-right[ .center[   ] ] --- # A Reminder: It's Demand all the Way Down! .pull-left[ - .hi-red[Supply] is actually .hi-blue[Demand] in disguise! - An .hi[(opportunity) cost] to buy (scarce) inputs for production because **other people** .hi-blue[demand] those same inputs to consume or produce **other valuable things**! - Price necessary to **pull them out of other valuable productive uses** in the economy! ] .pull-right[ .center[  ] ] --- # Production Costs are Opportunity Costs .pull-left[ - Because resources are scarce, and have rivalrous uses, .hi-turquoise[how do we know we are using resources efficiently??] - In functioning markets, .hi-purple[the market price measures the opportunity cost of using a resource for an alternative use] - Firms not only pay for direct use of a resource, but also indirectly compensate society for *“pulling the resource out”* of alternate uses in the economy! ] .pull-right[ .center[   ] ] --- # Production Costs are Opportunity Costs .pull-left[ - Every choice incurs an opportunity cost .bg-washed-green.b--dark-green.ba.bw2.br3.shadow-5.ph4.mt5[ .green[**Examples**]: .smallest[ - If you start a business, you may give up your salary at your current job - If you invest in a factory, you give up other investment opportunities - If you use an office building you own, you cannot rent it to other people - If you hire a skilled worker, you must pay them a high enough salary to deter them from working for other firms ] ] ] .pull-right[ .center[  ] ] --- # Opportunity Costs vs. Sunk Costs .pull-left[ - Opportunity cost is a *forward-looking* concept - Choices made in the *past* with *non-recoverable* costs are called .hi[sunk costs] - Sunk costs *should not* enter into future decisions - Many people have difficulty letting go of unchangeable past decisions: .hi-purple[sunk cost fallacy] ] .pull-left[ .center[  ] ] --- # Common Sunk Costs in Business .pull-left[ - Licensing fees, long-term lease contracts - Specific capital (with no alternative use): uniforms, menus, signs - Research & Development spending - Advertising spending ] .pull-right[ .center[  ] ] --- # The Accounting vs. Economic Point of View I .pull-left[ - Helpful to consider two points of view: 1. .hi-purple[“Accounting point of view”]: are you taking in more cash than you are spending? 2. .hi[“Economic point of view”]: is your product you making the *best social* use of your resources - i.e. are there higher-valued uses of your resources you are keeping them out of? ] .pull-right[ .center[   ] ] --- # The Accounting vs. Economic Point of View II .pull-left[ .smaller[ - .hi-turquoise[Implications for society]: are consumers *best* off with you using scarce resources (with alternative uses!) to produce your current product? - Remember: .hi-turquoise[this is an .ul[*economics*] course, not a *business* course]! - .hi-purple[Economists are pro-market, *not* pro-business!] - What might be good/bad for **one** business might have bad/good *consequences* for society! ] ] .pull-right[ .center[   ] ] --- class: inverse, center, middle # Costs in the Short Run --- # Costs in the Short Run - .hi[Total cost function, `\\(C(q)\\)`] relates output `\(q\)` to the total cost of production `\(C\)`<sup>.magenta[†]</sup> `$$C(q)=f+VC(q)$$` -- - Two kinds of short run costs: **1.** .hi[Fixed costs, `\\(f\\)`] are costs that do not vary with output - Only true in the short run! (Consider this the cost of maintaining your capital) -- **2.** .hi[Variable costs, `\\(VC(q)\\)`] are costs that vary with output (notice the variable in them!) - Typically, the more production of `\(q\)`, the higher the cost - e.g. firm is hiring *additional* labor .source[<sup>.magenta[†]</sup> Assuming that (i) firms are always choosing input combinations that minimize total cost and (ii) input prices are constant. See more in [today’s appendix](/resources/appendices/2.4-appendix.html).] --- # Fixed vs. Variable costs: Examples .pull-left[ .center[  ] ] .pull-right[ .bg-washed-green.b--dark-green.ba.bw2.br3.shadow-5.ph4.mt5[.hi-green[Example]: Airlines **Fixed costs**: the aircraft, regulatory approval **Variable costs**: providing one more flight ] ] --- # Fixed vs. Variable costs: Examples .pull-left[ .center[  ] ] .pull-right[ .bg-washed-green.b--dark-green.ba.bw2.br3.shadow-5.ph4.mt5[.hi-green[Example]: Car Factory **Fixed costs**: the factory, machines in the factory **Variable costs**: producing one more car ] ] --- # Fixed vs. Variable costs: Examples .pull-left[ .center[  ] ] .pull-right[ .bg-washed-green.b--dark-green.ba.bw2.br3.shadow-5.ph4.mt5[.hi-green[Example]: Starbucks **Fixed costs**: the retail space, espresso machines **Variable costs**: selling one more cup of coffee ] ] --- # Fixed vs. Sunk costs .pull-left[ .smallest[ - Diff. between .hi[fixed] vs. .hi-purple[sunk] costs? - .hi-purple[Sunk costs] are a *type* of .hi[fixed cost] that are *not* avoidable or recoverable - Many .hi[fixed costs] can be avoided or changed in the long run - Common .hi[fixed], but *not* .hi-purple[sunk], costs: - rent for office space, durable equipment, operating permits (that are renewed) - When deciding to *stay* in business, .hi[fixed costs] matter, .hi-purple[sunk costs] do not! ] ] .pull-right[ .center[  ] ] --- # Cost Functions: Example, Visualized .pull-left[ .tiny[ | `\(q\)` | `\(f\)` | `\(VC(q)\)` | `\(C(q)\)` | |----:|----:|--------:|-------:| | `\(0\)` | `\(10\)` | `\(0\)` | `\(10\)` | | `\(1\)` | `\(10\)` | `\(2\)` | `\(12\)` | | `\(2\)` | `\(10\)` | `\(6\)` | `\(16\)` | | `\(3\)` | `\(10\)` | `\(12\)` | `\(22\)` | | `\(4\)` | `\(10\)` | `\(20\)` | `\(30\)` | | `\(5\)` | `\(10\)` | `\(30\)` | `\(40\)` | | `\(6\)` | `\(10\)` | `\(42\)` | `\(52\)` | | `\(7\)` | `\(10\)` | `\(56\)` | `\(66\)` | | `\(8\)` | `\(10\)` | `\(72\)` | `\(82\)` | | `\(9\)` | `\(10\)` | `\(90\)` | `\(100\)` | | `\(10\)` | `\(10\)` | `\(110\)` | `\(120\)` | ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-14-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Average Costs - .hi[Average Fixed Cost]: fixed cost per unit of output: `$$AFC(q)=\frac{f}{q}$$` -- - .hi[Average Variable Cost]: variable cost per unit of output: `$$AVC(q)=\frac{VC(q)}{q}$$` -- - .hi[Average (Total) Cost]: (total) cost per unit of output: `$$AC(q)=\frac{C(q)}{q}$$` --- # Marginal Cost - .hi[Marginal Cost] is the change in total cost for each additional unit of output produced: `$$MC(q) = \frac{\Delta C(q)}{\Delta q}$$` - Calculus: first derivative of the cost function - .hi-purple[Marginal cost is the *primary* cost that matters in making decisions] - All other costs are driven by marginal costs - This is the main cost that firms can “see” --- # Average and Marginal Costs: Visualized .center[ <img src="1.2-slides_files/figure-html/unnamed-chunk-15-1.png" width="1008" style="display: block; margin: auto;" /> ] --- # Relationship Between Marginal and Average .pull-left[ .smallest[ - Mathematical relationship between a marginal & an average value - If .red[marginal] `\(<\)` .orange[average], then .orange[average] `\(\downarrow\)` ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-16-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Relationship Between Marginal and Average .pull-left[ .smallest[ - Mathematical relationship between a marginal & an average value - If .red[marginal] `\(<\)` .orange[average], then .orange[average] `\(\downarrow\)` - If .red[marginal] `\(>\)` .orange[average], then .orange[average] `\(\uparrow\)` ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-17-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Relationship Between Marginal and Average .pull-left[ .smallest[ - Mathematical relationship between a marginal & an average value - If .red[marginal] `\(<\)` .orange[average], then .orange[average] `\(\downarrow\)` - If .red[marginal] `\(>\)` .orange[average], then .orange[average] `\(\uparrow\)` - When .red[marginal] `\(=\)` .orange[average], .orange[average] is **maximized/minimized** ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-18-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Relationship Between Marginal and Average .pull-left[ .smallest[ - Mathematical relationship between a marginal & an average value - If .red[marginal] `\(<\)` .orange[average], then .orange[average] `\(\downarrow\)` - If .red[marginal] `\(>\)` .orange[average], then .orange[average] `\(\uparrow\)` - When .red[marginal] `\(=\)` .orange[average], .orange[average] is **maximized/minimized** - .hi-purple[When MC(q)=AC(q), AC(q) is at a *minimum*] (break-even price) - .hi-purple[When MC(q)=AVC(q), AVC(q) is at a *minimum*] (shut-down price) ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-19-1.png" width="504" style="display: block; margin: auto;" /> ] --- class: inverse, center, middle # Costs in the Long Run --- # Costs in the Long Run .pull-left[ - .hi[Long run]: firm can change all factors of production & vary scale of production - .hi-purple[Long run average cost, LRAC(q)]: cost per unit of output when the firm can change *both* `\(l\)` and `\(k\)` to make more `\(q\)` - .hi-purple[Long run marginal cost, LRMC(q)]: change in long run total cost as the firm produce an additional unit of `\(q\)` (by changing *both* `\(l\)` and/or `\(k\)`) ] .pull-right[ .center[  ] ] --- # Average Cost in the Long Run .pull-left[ - .hi[Long run]: firm can choose `\(k\)` (factories, locations, etc) - Separate short run average cost (SRAC) curves for each amount of `\(k\)` potentially chosen ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-20-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Average Cost in the Long Run .pull-left[ - .hi[Long run]: firm can choose `\(k\)` (factories, locations, etc) - Separate short run average cost (SRAC) curves for each amount of `\(k\)` potentially chosen - .hi-purple[Long run average cost (LRAC)] curve “envelopes” the lowest (optimal) regions of all the SRAC curves! .smallest[ > “Subject to producing the optimal amount of output, choose l and k to minimize cost” ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-21-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Long Run Costs & Scale Economies I .pull-left[ .center[  ] ] .pull-right[ .quitesmall[ - Further important properties about costs based on .hi[scale economies] of production: change in **average costs** when output is increased (scaled) - .hi-purple[Economies of scale]: average costs .hi-turquoise[fall] with more output - High fixed costs `\(AFC > AVC(q)\)` low variable costs - .hi-purple[Diseconomies of scale]: average costs .hi-turquoise[rise] with more output - Low fixed costs `\(AFC < AVC(q)\)` high variable costs - .hi-purple[Constant economies of scale]: average costs .hi-turquoise[don’t change] with more output - Firm at minimum average cost (optimal plant size), called .hi[minimum efficient scale (MES)] ] ] --- # Long Run Costs & Scale Economies II .pull-left[ - .hi[Minimum Efficient Scale]: `\(q\)` with the lowest `\(AC(q)\)` - “optimal firm size” ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-22-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Long Run Costs & Scale Economies II .pull-left[ - .hi[Minimum Efficient Scale]: `\(q\)` with the lowest `\(AC(q)\)` - “optimal firm size” - .hi-green[Economies of Scale]: `\(\uparrow q\)`, `\(\downarrow AC(q)\)` ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-23-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Long Run Costs & Scale Economies II .pull-left[ - .hi[Minimum Efficient Scale]: `\(q\)` with the lowest `\(AC(q)\)` - “optimal firm size” - .hi-green[Economies of Scale]: `\(\uparrow q\)`, `\(\downarrow AC(q)\)` - .hi-red[Diseconomies of Scale]: `\(\uparrow q\)`, `\(\uparrow AC(q)\)` ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-24-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Long Run Costs & Scale Economies III .pull-left[ - Can measure economies of scale `\((S)\)`: `$$S(q) = \frac{AC(q)}{MC(q)}$$` - `\(S>1\)`: economies of scale at `\(q\)` - `\(S<1\)`: diseconomies of scale at `\(q\)` - `\(S=1\)`: minimum efficient scale at `\(q\)` ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-25-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Economies of Scope .pull-left[ - We often assume .hi[single-product plants/firms], but in reality most firms/plants are .hi[multi-product] - .hi[Economies of Scope]: cost of producing multiple products (e.g. `\(q_1\)` and `\(q_2\)`) in a single plant exceeds costs of producing a single product in each plant `$$C(q_1,q_2) < C(q_1,0)+C(0,q_2)$$` ] .pull-right[ .center[  ] ] --- class: inverse, center, middle # Revenues --- # Revenues for Firms in *Competitive* Industries I .pull-left[ <img src="1.2-slides_files/figure-html/unnamed-chunk-26-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ <img src="1.2-slides_files/figure-html/industry-graph-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Revenues for Firms in *Competitive* Industries I .pull-left[ <img src="1.2-slides_files/figure-html/unnamed-chunk-27-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-28-1.png" width="504" style="display: block; margin: auto;" /> ] -- - .blue[Demand for a firm’s product] is **perfectly elastic** at the market price -- - Where did the .red[supply curve] come from? You’ll know today --- # Revenues for Firms in *Competitive* Industries II .pull-left[ <img src="1.2-slides_files/figure-html/unnamed-chunk-29-1.png" width="504" style="display: block; margin: auto;" /> ] .pull-right[ - .hi[Total Revenue] `\(R(q)=pq\)` ] --- # Average and Marginal Revenues - .hi[Average Revenue]: revenue per unit of output `$$AR(q)=\frac{R}{q}$$` - `\(AR(q)\)` is **by definition** equal to the price! (Why?) -- - .hi[Marginal Revenue]: change in revenues for each additional unit of output sold: `$$\color{#e64173}{MR(q) = \frac{\Delta R(q)}{\Delta q}}$$` - Calculus: first derivative of the revenues function - .hi-purple[For a .ul[*competitive*] firm (only), MR(q) = p, i.e. the price!] --- # Average and Marginal Revenues: Example .bg-washed-green.b--dark-green.ba.bw2.br3.shadow-5.ph4.mt5[ .green[**Example**]: A firm sells bushels of wheat in a very competitive market. The current market price is .blue[$10/bushel]. ] -- .pull-left[ For the 1<sup>st</sup> bushel sold: - What is the total revenue? - What is the average revenue? ] -- .pull-right[ For the 2<sup>nd</sup> bushel sold: - What is the total revenue? - What is the average revenue? - What is the marginal revenue? ] --- # Total Revenue, Example: Visualized .pull-left[ .quitesmall[ | `\(q\)` | `\(R(q)\)` | |----:|-------:| | `\(0\)` | `\(0\)` | | `\(1\)` | `\(10\)` | | `\(2\)` | `\(20\)` | | `\(3\)` | `\(30\)` | | `\(4\)` | `\(40\)` | | `\(5\)` | `\(50\)` | | `\(6\)` | `\(60\)` | | `\(7\)` | `\(70\)` | | `\(8\)` | `\(80\)` | | `\(9\)` | `\(90\)` | | `\(10\)` | `\(100\)` | ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-30-1.png" width="504" style="display: block; margin: auto;" /> ] --- # Average and Marginal Revenue, Example: Visualized .pull-left[ .quitesmall[ | `\(q\)` | `\(R(q)\)` | `\(AR(q)\)` | `\(MR(q)\)` | |----:|-------:|--------:|--------:| | `\(0\)` | `\(0\)` | `\(-\)` | `\(-\)` | | `\(1\)` | `\(10\)` | `\(10\)` | `\(10\)` | | `\(2\)` | `\(20\)` | `\(10\)` | `\(10\)` | | `\(3\)` | `\(30\)` | `\(10\)` | `\(10\)` | | `\(4\)` | `\(40\)` | `\(10\)` | `\(10\)` | | `\(5\)` | `\(50\)` | `\(10\)` | `\(10\)` | | `\(6\)` | `\(60\)` | `\(10\)` | `\(10\)` | | `\(7\)` | `\(70\)` | `\(10\)` | `\(10\)` | | `\(8\)` | `\(80\)` | `\(10\)` | `\(10\)` | | `\(9\)` | `\(90\)` | `\(10\)` | `\(10\)` | | `\(10\)` | `\(100\)` | `\(10\)` | `\(10\)` | ] ] .pull-right[ <img src="1.2-slides_files/figure-html/unnamed-chunk-31-1.png" width="504" style="display: block; margin: auto;" /> ]